Why token prices may fall when users create value but holders get nothing back

Many crypto tokens follow the same pattern.

They launch with strong hype.

Early investors get excited.

The token lists on exchanges.

Then, after a short period, the price starts falling.

For a long time, people blamed bad market conditions, weak communities, or venture capital unlocks. But Arthur Hayes, co-founder of BitMEX, has offered a much sharper view.

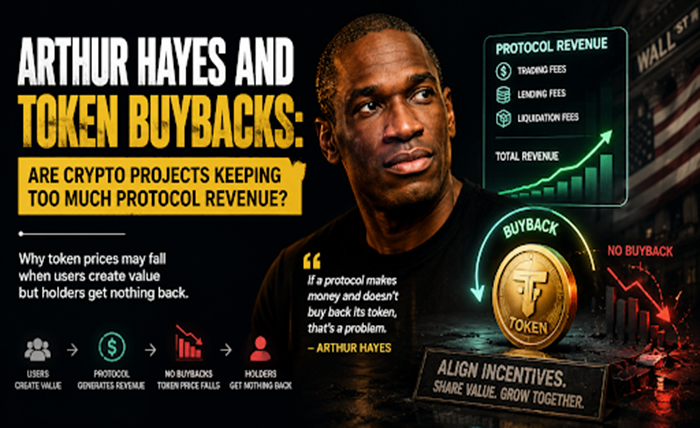

In May 2026, Hayes argued that many crypto tokens fall because projects do not return protocol-level economic value to token holders. Instead, revenue often stays with teams, treasuries, insiders, or other parts of the project structure. He also said venture investors may sell after unlocks because they have a duty to return capital to their own investors.

So, is token price weakness really caused by projects keeping too much revenue?

Let’s break it down.

Why Arthur Hayes Is Talking About Token Value

Arthur Hayes is known for making strong market arguments.

His point is simple: a token needs a reason to go up besides hype. If a protocol creates real revenue but the token does not receive any of that value, then holders are only betting that someone else will buy later.

That is not a strong long-term model.

In traditional markets, investors often look at cash flow, earnings, dividends, and buybacks. In crypto, many tokens have none of these. They may have governance rights, community value, or staking features, but they may not have a direct link to protocol revenue.

This creates a problem.

If insiders and early investors sell over time, but the token has no buyback or revenue-sharing support, the market may face constant selling pressure.

What Is a Token Buyback?

A Token buyback happens when a project uses revenue or treasury funds to buy its own token from the open market.

This can create real buying pressure.

It can also show that the project is trying to return value to token holders. In simple terms, if a protocol earns fees and uses part of those fees to buy the token, then the token has a clearer connection to the project’s business activity.

Hayes often points to Hyperliquid as an example. In his own March 2026 essay, he wrote that Hyperliquid uses about 97% of its revenue to buy back HYPE tokens from the market, and he described it as one of the strongest value-return models in crypto.

This is why buybacks are becoming an important topic.

Why Many Tokens Keep Falling

Many crypto projects launch tokens before they have strong revenue.

At the beginning, there is excitement. The community talks about future adoption. Exchanges list the token. Early backers are still locked, so selling pressure may look low.

But later, unlocks begin.

Team tokens unlock.

VC tokens unlock.

Market makers manage liquidity.

Retail demand slows down.

Revenue does not flow to holders.

When this happens, the token can fall even if the product is still active.

That is the core of Hayes’ argument. The problem is not always that the project has no users. The problem is that token holders may not benefit from those users.

Is Revenue Hoarding the Real Problem?

It can be part of the problem.

Projects do need money to operate. They must pay developers, security teams, legal costs, marketing expenses, and ecosystem grants. Not every dollar can go to token holders.

But if a protocol earns meaningful revenue and none of it supports the token, investors may start asking harder questions.

Who benefits from the protocol?

Does the token capture value?

Are buybacks real or only marketing?

Do holders get anything besides governance?

Will unlocks create more selling pressure?

These questions matter because crypto investors are becoming more mature. They no longer want only a white paper and a strong investor list. They want real cash flow and better token design.

Final Thoughts

Arthur Hayes’ argument is uncomfortable, but important.

Many tokens may not fall only because of bad market conditions. They may fall because the token has no clear link to the revenue created by the protocol.

That does not mean every project must use the same model. Some protocols may need to reinvest revenue. Others may prefer staking rewards, fee sharing, burns, or treasury growth.

But the direction is clear.

Crypto investors are starting to care more about value capture. Token buybacks, revenue sharing, and transparent treasury policies may become more important in the next market cycle.

The projects that survive may not be the ones with the loudest launch.

They may be the ones that prove their token is more than an exit vehicle.